Innovation in emergencies: the launch of 'mobile money' in Haiti

- Issue 54 New learning in cash transfer programming

- 1 Bigger, better, faster: achieving scale in emergency cash transfer programmes

- 2 'More than just another tool': a report on the Copenhagen Cash and Risk Conference

- 3 Cash transfers and response analysis in humanitarian crises

- 4 A deadly delay: risk aversion and cash in the 2011 Somalia famine

- 5 Institutionalising cash transfer programming

- 6 New technologies in cash transfer programming and humanitarian assistance

- 7 Innovation in emergencies: the launch of 'mobile money' in Haiti

- 8 Lessons learnt on unconditional cash transfers in Haiti

- 9 Fresh food vouchers: findings of a meta-evaluation of five fresh food voucher programmes

- 10 Bridging the gap between policy and practice: the European Consensus on Humanitarian Aid and Humanitarian Principles

- 11 Humanitarian financing and older people

- 12 The rehabilitation response in Haiti: a systems evaluation approach

- 13 Working with Somali diaspora organisations in the UK

- 14 Applying conflict-sensitive methodologies in rapid-onset emergencies

Rapid-onset emergencies are not contexts where one would expect to see innovation. The scale of devastation requires focused and fast action. Emergency professionals apply standard operating procedures and proven methodologies from previous humanitarian responses, and there is no time to develop and test innovative solutions effectively. Yet it could also be argued that crisis situations open up opportunities that make lasting change possible. Considering non-traditional solutions is easier because the disaster highlights that business as usual is no longer an option.

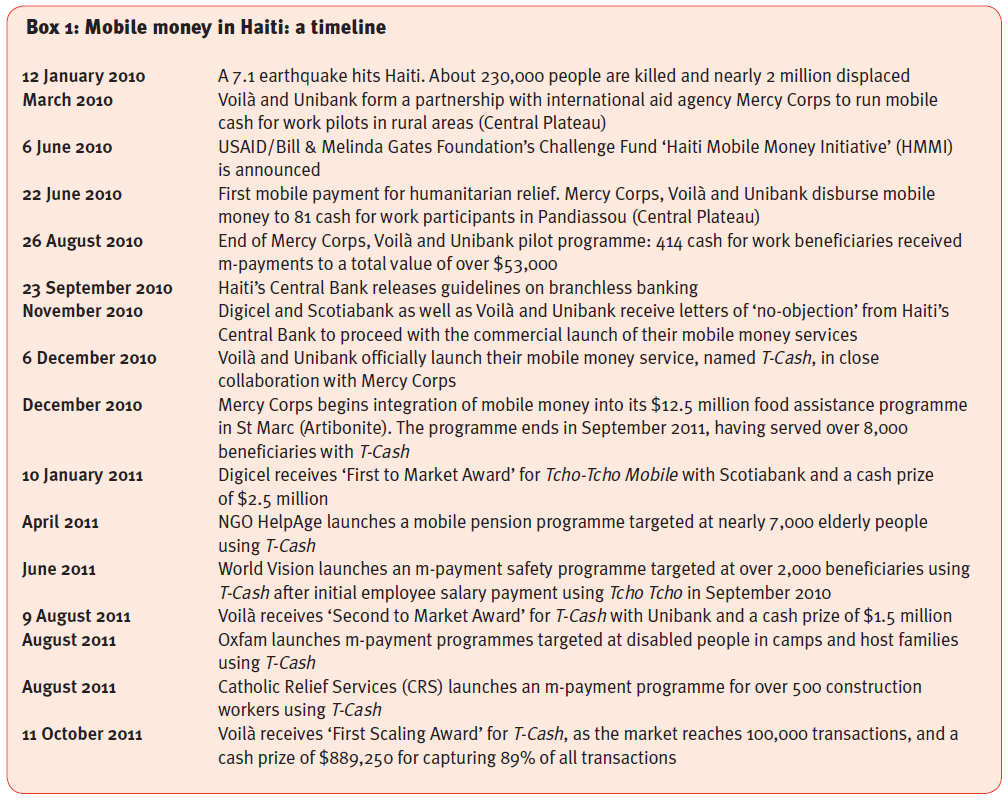

The introduction of mobile money following the devastating earthquake in Haiti in January 2010 is an important example of innovation in an emergency. Humanitarian aid channelled through cash transfer programmes helped foster innovation in electronic payments, in a country severely lacking in financial infrastructure. There are a growing number of examples of the use of mobile technologies in humanitarian response, including in Kenya and Niger. J. C. Aker, R. Boumnijel, A. McClelland and N. Tierney, Zap It To Me: The Short-Term Impacts of a Mobile Cash Transfer Program, Working Paper 268, Centre for Global Development, 2011. However, what makes Haiti so special is that, as the country struggled with large-scale emergency response, mobile money services and the framework required to regulate them were developed simultaneously. Mobile money proved not only useful for the immediate humanitarian context, but also, when coupled with financial education, for the longer-term goal of providing financial access to the unbanked those outside of the banking system.

What is mobile money?

Mobile money is electronic currency stored in an electronic wallet on a mobile phone. This can be converted back into cash with designated agents at any time, and used to purchase goods or pay bills at affiliated merchants, or transfer money to other individuals. The e-wallet is protected by a personal identification number (PIN), and accounts are debited or credited as soon as the transaction takes place. Mobile money has been particularly useful in developing countries where access to formal financial services is limited, and transferring money between urban and rural areas is difficult. Mobile money allows people to bank at post offices, stores and other suitable outlets in the local community, which act as banking agents. In Haiti, mobile money systems followed a bank-led model, which consisted of a partnership between a bank and a mobile network operator (MNO). Two MNOs dominate the market, Digicel, which chose to partner with Scotiabank to roll out a mobile money service called Tcho Tcho, and Voilà, which worked with Unibank to launch T-Cash.

The cash response

The emergency response in Haiti was characterised by a very high level of cash-based interventions, in particular cash-for-work and cash grants. Despite the massive destruction, local markets began functioning again shortly after the earthquake, prompting the government to stop direct food distributions within three months. The lack of automatic teller machines (ATMs) and point-of-sale terminals in stores discouraged the use of smart cards by aid agencies. More traditional delivery mechanisms, such as distributing cash in envelopes, collections at bank branches and the use of money transfer agents, were common, but most financial service points in Haiti are concentrated in and around the capital Port-au-Prince, making access to financial services in rural areas very difficult.

Six months after the earthquake, in June 2010, USAID and the Gates Foundation announced a Challenge Fund Competition to encourage the launch of mobile money services in Haiti and to expedite the delivery of cash assistance to victims of the countrys devastating earthquake by humanitarian agencies. See http://www.gatesfoundation.org/press-releases/Pages/building-assets-with-mobile-money-service-in-haiti-100608.aspx. The intent to use the humanitarian intervention to bring about innovation in financial services was clear. While opinions vary on whether a prize mechanism was appropriate, and whether it succeeded in delivering high-quality, sustainable products, the competition elicited a favourable response from the Banque de la République dHaiti (BRH Haitis Central Bank) and accelerated the development of regulatory guidelines for mobile money and branchless banking at large. The BRH allowed a flexible approach to customer registration based on a tiered Know-Your-Customer (KYC) system. This meant that subscribers could access and store as much as $60 on their phone without providing additional identification beyond what is required to register a SIM card. For higher limits (up to $250), full identification is required. This first-tier KYC (or mini-wallet as it was commonly called) was particularly relevant for NGO programmes whose cash for work payments rarely exceeded $60.

Programme design for mobile transfer differs little from programmes distributing cash in other ways (e.g. in envelopes). The mobile process generally consists of loading the NGOs disbursement account with e-money through a bank transfer from the national bank account. Then, instead of sending beneficiaries names and payment instructions to the finance department or transfer agent, programme managers access an online platform and send the payment notification to beneficiaries mobile phones. Beneficiaries then go to a nearby agent to collect their cash.

Programme design for mobile transfer differs little from programmes distributing cash in other ways (e.g. in envelopes). The mobile process generally consists of loading the NGOs disbursement account with e-money through a bank transfer from the national bank account. Then, instead of sending beneficiaries names and payment instructions to the finance department or transfer agent, programme managers access an online platform and send the payment notification to beneficiaries mobile phones. Beneficiaries then go to a nearby agent to collect their cash.

An added benefit is that beneficiaries need not collect their payment in full. Instead, they can keep a residual balance on their e-wallet and thus better manage their expenditure. Safe storage of money was invaluable for many beneficiaries displaced in camps after the earthquake. In addition, options such as balance checks and mini-statements are available, allowing people to track their transaction history, which could be very valuable in future negotiations with lenders, while financial literacy training can improve money management. Success need not necessarily be measured in the sustained adoption of mobile money, but in improved financial management and the use of additional formal financial services by the poor.

Other benefits identified by programme beneficiaries included:

- Increased security as the e-wallet is protected by a PIN.

- Reduced transaction costs: no need to stand in line to collect payments at cash for work sites.

- Privacy: payment notification takes the form of a text message on a personal phone, so there is little outside knowledge of the payment, reducing rent-seeking from cash for work team leaders and unwanted debt collections from creditors on pay day.

- Convenience: the system is real-time, accessible 24 hours a day and increasingly widely available as the agent network grows.

- Speed: transactions can be as short as 60 seconds depending on the beneficiarys proficiency with the system.

- Use of technology: often described as a major source of pride to many rural poor.

For NGOs, mobile money can:

- Reduce operational costs, especially when the same beneficiary group needs to receive recurrent payments.

- Reduce logistics and improve programme efficiency.

- Mitigate some of the risks associated with cash transfers, especially security and liquidity management.

- Provide direct contact with beneficiaries through mobile phones, allowing for more communication potentially leading to increased accountability.

- Increase the capacity of beneficiaries to use financial systems.

Challenges

The challenges of implementing mobile money programmes are, however, still significant. NGOs that used mobile money in their humanitarian response in Haiti were faced with a complex, high-profile emergency, a nascent mobile money ecosystem and an evolving regulatory framework. Introducing mobile money into cash programming first required an institutional shift. Some emergency responders and cash transfer professionals resisted the new methodology. For example, finance officers argued against electronic payments because they did not have a way of acknowledging receipt of payment. Commitment at both HQ and field level was essential for moving forward.

Faced with the challenge that some beneficiaries lacked phones, programme managers had to decide whether to give out handsets or SIM cards only. Deciding which carrier to use, or indeed whether a mixed carrier approach was viable, was another key question. Meeting regulatory requirements in terms of user identification was easy enough in Haiti thanks to the mini-wallet. The challenge of providing product orientation and beneficiary training, especially to non-literate/numerate beneficiaries, was often overcome by using pictures and role play. Mobile providers offered extensive support to beneficiary training.

Agent presence and liquidity were other major issues. To guarantee adequate service provision, service providers had to simultaneously build a strong pool of early adopters on the demand side and the required agent network on the supply side. They needed enough users demanding their service to incentivise agents to get on board, as well as enough agents to motivate users to sign up. However, they had difficulty growing the mobile money ecosystem at the pace and scale required to meet the demands of humanitarian agencies, especially in under-served rural areas, making it difficult to reach beneficiaries. Close collaboration between NGOs and service providers was required to ensure adequate network coverage in intervention areas, as well as advance warning to allow agents to plan their liquidity reserves to meet cash transfer timings.

What is so impressive in Haiti is the sheer number of mobile cash transfer programmes NGOs have implemented since the launch of T-Cash and Tcho Tcho (eight out of 14 such programmes worldwide). See http://www.ssireview.org/pdf/120119_HMMI_-_Plugging_Into_Mobile_Money_Platforms_FINAL2.pdf. The programmes in Haiti were implemented by NGOs with varying degrees of familiarity with electronic payments, and included a wide range of beneficiaries (urban displaced (CRS), the elderly (Help Age), rural displaced (Mercy Corps) and camp residents and host families (Oxfam GB)). These humanitarian programmes, along with the USAID/Gates Foundation prize, contributed significantly to the rapid growth of Haitis mobile money ecosystem, making it the most successful mobile money deployment in Latin America and the Caribbean. See http://www.movilion.com/good-news-from-haiti-first-success-story-for-the-mobile-wallet-in-latin-america-and-the-caribbean. Haiti shows that innovation and emergencies are not incompatible. On the contrary, emergencies present a tremendous opportunity to innovate and to advocate for more daring response methodologies. Innovation need not be the bold introduction of an earth-shattering invention, but simply the smart application of a new or less-used solution.

Kokoévi Sossouvi was the Economic Recovery Programme Manager for Mercy Corps in Haiti from March 2010 until August 2011. She is currently Director of Strategic Partnerships at the Voilà Foundation in Haiti.

Comments

Thanks for choosing to leave a comment. Please keep in mind that all comments are moderated according to our comment policy.

Let’s have a personal and meaningful conversation.